Dividend Stock Analysis of Kroger (KR)

The Kroger Co. (KR) operates as a retailer in the United States. The company operates supermarkets, multi-department stores, marketplace stores, and price impact warehouse stores.

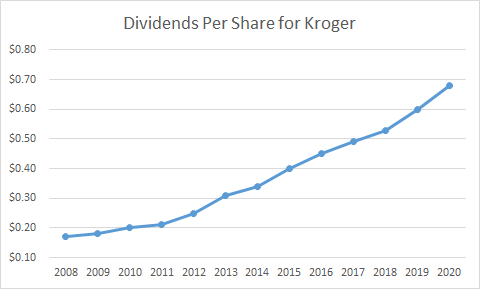

Kroger is a dividend achiever, which recently hiked quarterly dividends by 16.70% to 21 cents/share. This marked the 15th consecutive year of annual dividend increases for the company.

Warren Buffett has also been slowly building up a position in Kroger.

During the past decade, Kroger has managed to grow dividends at an annualized rate of 12.60%.

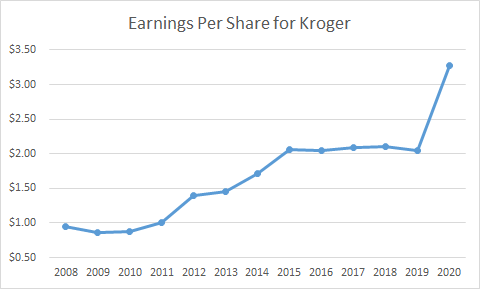

Kroger managed to grow earnings per share from 95 cents/share in 2008 to $3.27/share in 2020. The 2018 numbers are adjusted to exclude the gain on sale of Kroger’s convenience store business. The company expects to generate between $2.95 - $3.10/share in 2021.

Last year was a nice bump in earnings, given the fact that earnings per share had gone nowhere since 2015. That was due to investments in the company’s business going forward. It appears that earnings may go lower in 2021 as fewer consumers stock up on goods like they did at the beginning of the pandemic.

Kroger's financial strategy is to use its free cash flow to drive growth while also maintaining its current investment grade debt rating and returning capital to shareholders. The company actively balances the use of its cash flow to achieve these goals.

The grocery business is highly competitive, with Kroger competing against the likes of Wal-Mart and Target, as well as mom and pop grocery stores, as well as the likes of Amazon. The company needs to continuously invest in stores, drive efficient operations, new products and innovation ( such as online, and delivery/pick up). Kroger does have the scale of operations to effectively compete, and also has attractive store locations. This allows it to be able to do online purchase and pick up at 57% of its stores and home delivery for 91% of customers. Back in 2018, Kroger invested in Ocado, which is its exclusive grocery delivery partner in the US. Ocado delivers groceries in Europe. Kroger has also made investments in new warehouses, store optimization, expanding its own private label brands and digital, in an effort to drive long-term sales growth. Same store sales growth and cost reductions are the drivers that will propel earnings per share growth over time.

Kroger is also competing by offering a large variety of private label brands that it owns and manufactures internally. This allows it to generate very good profit margins on these items relative to branded products.

Kroger also competes by including pharmacies in order three-quarters of its stores and a gas station in over half of its locations. Customers who fill in a prescription by getting in the store are also likely to make another purchase or two. The same goes for customers who would appreciate the convenience of shopping for gas, filling prescriptions and doing their grocery shopping.

Kroger is also planning to develop alternative revenue streams using the data it collects on shoppers, targeting personal finance products and media ad revenues. The company collects a lot of date on customers that shop there, which can also be used as a tool to provide a more personalized shopping experience. Another alternative revenue stream is the Home Chef meal delivery service, which provides ingredients for meals in 48 states in the United States. Kroger acquired Home Chef in 2018, and the meal kits are available at Kroger locations, including a few Walgreen’s stores.

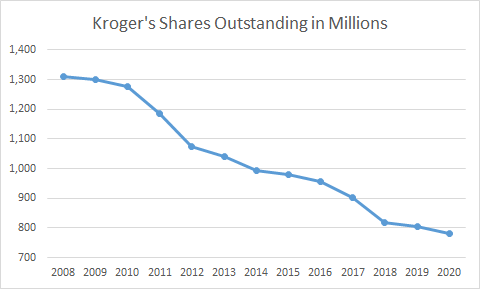

Kroger has rewarded shareholders handsomely with dividends and share buybacks. Between 2008 and 2020, the number of shares outstanding has gone down from 1.31 billion shares to 781 million shares. This means that shareholders from 2008, who stayed invested in Kroger, increased their ownership in the company by two-thirds without doing anything.

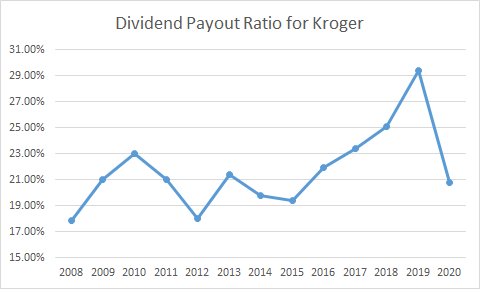

The dividend payout ratio increased from 17.90% in 2008 to 20.80% in 2020. A lower payout ratio provides an adequate margin of safety in the dividend payment, which can provide protection against short-term turbulence in earnings per share. There is room for increase in the payout ratio from here. Future dividend growth can be helped by a gradual increase in the payout ratio. If Kroger is unable to jump start earnings growth however, there will be a natural limit to further dividend growth. I would get worried if earnings are not growing, but dividends are, and the payout ratio exceeds 60%

Currently the stock is attractively valued at 12.83 times forward earnings and offer an attractive dividend yield of 2.10%.

Relevant Articles:

- Three Dividend Achievers Distributing More Cash to Shareholders

- Does Paying a Dividend Reduce a Company’s Value?

- Attractively Valued Dividend Contenders To Consider

- Supervalu (SVU) Dividend Stock Analysis